Although I made a case for a pullback in crude oil along with a pullback in the energy sector when ERX/XLE was added as a short trade idea on Thursday, it was not an oversight that USO or any other proxies for trading crude oil were not also added as Active Short Trade ideas. Although I still believe that we are likely to see a false break/bull trap in crude oil, with USO briefly trading above the aforementioned basing pattern (which has started to occur today), my preference to short the oil & gas stocks vs. crude oil lies largely in the same reasoning that I provided as to why the unstoppable, almighty AAPL is likely to get dragged down, kicking & screaming, should my call for a substantial correction in the broad market occur soon.

I recently received this question regarding AAPL & my bearish outlook for the broad markets: Doesn’t the fact Apple is such a large part of the QQQ make you nervous though, with the fundamentals and earnings coming out… and given the fact that the stock has not really broken down in any significant way yet?

With my reply being: IF the market breaks down & starts selling off, AAPL will be sold too, regardless of fundies, due to forced selling. When the market sells off, the public panics and dumps their SPY, QQQ, mutual funds, 401k,etc… AAPL is the largest component and as such, forced selling will take place to meet redemptions.

The same principle holds true with XLE & the energy stocks. If even just a little air is squeezed out of this bubble in equity prices, as is most often the case, selling begets more selling. As the market begins to drop, first the momentum players begin to sell their long positions. After the first couple of support levels where the dip buyers try to step in get sliced through like they weren’t there, stops begin to get hit on both those who bought the dip as well as various other traders & investors, such as longs using trailing stops, Johnny-come-lately buyers who bought the top, etc.. Those sell orders, a large percentage of which are in index tracking etfs & mutual funds, are then processed by 401ks, mutual funds, etc…., all of which have T+business days to pay out the proceeds from those redemptions in cash.

In March, the liquidity ratio of equity funds (a ratio published monthly by the Investment Company Institute that compares the amount of cash relative to total assets held by a mutual fund)

fell to 3.5% from an already alarmingly (and bearish from a future potential supply/demand perspective) 3.6% in February (we are still awaiting the April data). What that means is that US equity funds have, by historical standards, very little cash on hand to meet customer redemptions OR to aggressively buy the next dip. Although we won’t know if the liquidity ratio of equity funds improved in April until those figures are released, we do know that the ICI reported net outflows of $13.7 billion in domestic (U.S.) equity funds over the past 4 weekly reporting periods which means that a good deal of any existing cash on-hand or possibly inflows during the month of April were used to meet those redemptions.

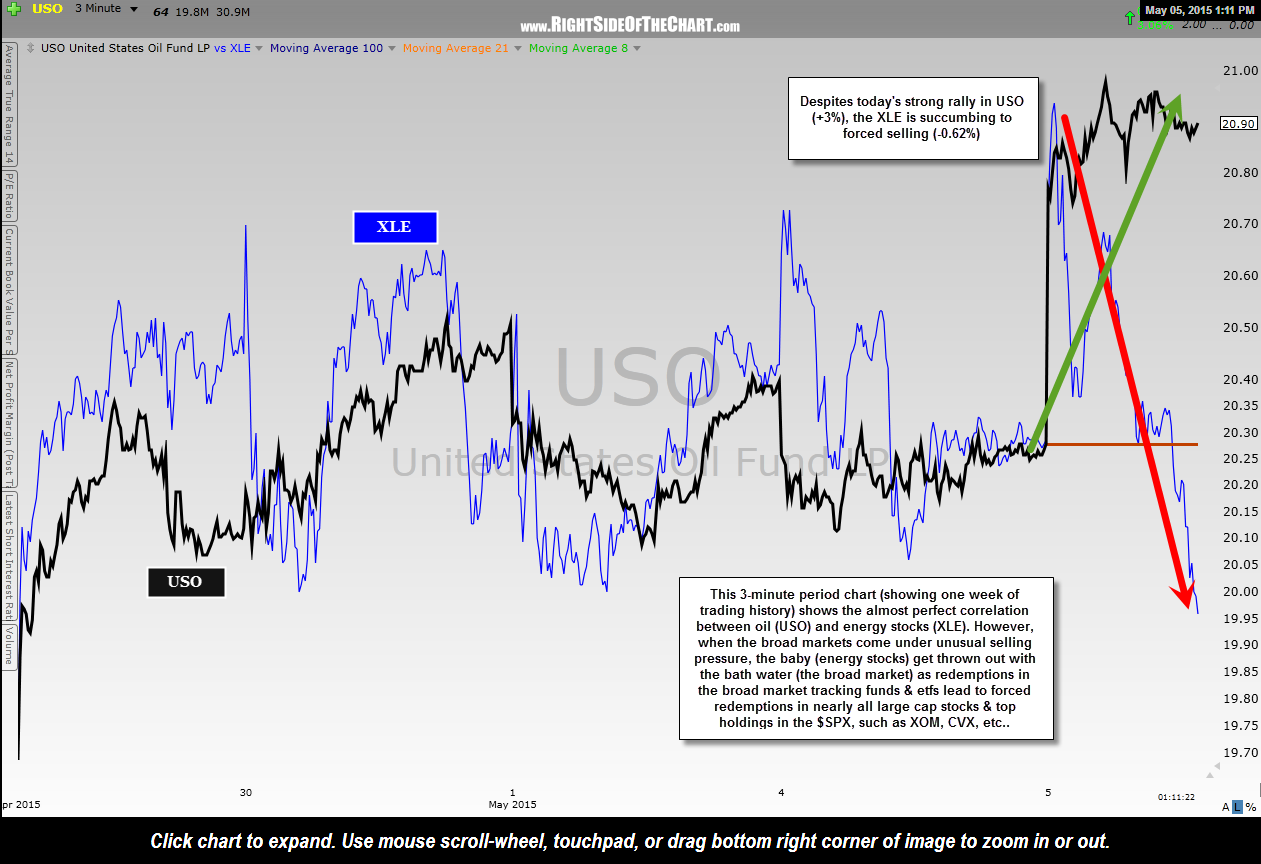

Enough on the supply/demand dynamics of the market, let’s get back to the fact that energy stocks are likely to fall with the market, at least for during periods of impulsive selling, despite what crude oil is doing. This 3-minute period chart (showing one week of trading history) shows the almost perfect correlation between oil (USO) and energy stocks (XLE); nearly perfect until today, that is. When the broad markets come under unusual selling pressure, the baby (energy stocks) gets thrown out with the bath water (the broad market) as redemptions in the broad market tracking funds & etfs lead to forced redemptions in nearly all large cap stocks & top holdings in the $SPX, such as XOM, CVX, etc.., as clearly seems to be the case today with USO trading up over 3% while XLE is trading solidly in the red.

XLE vs. USO May 5th