The last time I recall so much incessant chatter & focus on a potential market moving event would have to be the Grexit fears a few years back with the big difference being that those worries (of potential fallout from a Greek exit of the Eurozone) was that the markets had priced in a good amount of the potential fallout from such an event, should it have occurred. This time around things are different as the S&P 500 has surged about 16% off the February lows & is only mere percentage points from both its 2016 highs as well as all-time highs. With that being said, I think that it is reasonable to assume that the market has pretty much put full faith in the recent polls and has priced in a REMAIN vote. If so, that leaves very little, if any room for an upside “surprise” rally and a potentially powerful sell-off, should we happen to get a LEAVE vote. Then again, that assumes logic and reason, something that this CB manipulated market has been lacking for years so I’ll just leave it at that & wait to see what happens over the next several trading sessions as it isn’t the news or outcome of a particular event that matters in trading & investing, rather it is only the market’s reaction to an event that matters.

Whether the vote is STAY or GO, my expectation is that, barring the typically post-news noise (volatility), which should subside in a day or so after the results are in, is that the focus on the markets will quickly move away from the Brexit vote and any potential fallout, back towards the most important factor IMO which is the marked deterioration in U.S. corporate & economic fundamentals.

There are two primary disciplines or methodologies for security selection (deciding what to buy & when to buy & sell it) in trading & investing: Fundamental Analysis (FA) and Technical Analysis (TA). The definitions of each, as per Investopedia.com are:

FUNDAMENTAL ANALYSIS: A method of evaluating a security that entails attempting to measure its intrinsic value by examining related economic, financial and other qualitative and quantitative factors. Fundamental analysts attempt to study everything that can affect the security’s value, including macroeconomic factors (like the overall economy and industry conditions) and company-specific factors (like financial condition and management). The end goal of performing fundamental analysis is to produce a value that an investor can compare with the security’s current price, with the aim of figuring out what sort of position to take with that security (underpriced = buy, overpriced = sell or short). This method of security analysis is considered to be the opposite of technical analysis.

TECHNICAL ANALYSIS: Technical analysis is a trading tool employed to evaluate securities and attempt to forecast their future movement by analyzing statistics gathered from trading activity, such as price movement and volume. Unlike fundamental analysts who attempt to evaluate a security’s intrinsic value, technical analysts focus on charts of price movement and various analytical tools to evaluate a security’s strength or weakness and forecast future price changes.

Typically, fundamental analysis is utilized by long-term buy & hold investors or fund managers, such as Warren Buffet, while technical analysis is primarily used by swing traders & active traders with shorter time horizons on their trades ranging from minutes to day, weeks & usually not much more than a few months. One of the biggest issues with using FA when actively trading is that fundamentals, even if your analysis is spot on, can take months & sometimes years to become fully reflected in the price of the security. With technical analysis, we are able to much more precisely identify our entry & exit points on a trade.

Although traders & investors employing technical analysis rely heavily on the use of charts, not all charts fall under the category of TA. I have put together an extensive compilation of charts below which fall under the category of Fundamental Analysis & clearly show a marked deterioration in US corporate & economic fundamentals. Long before discovering the “magic” of technical analysis, my background & primary focus was fundamental analysis; first as a business major in college, with degrees in both Multinational Business & Marketing, followed by a 12-year career as a stock broker before walking away from that career to pursue my life’s passion (technical analysis & stock trading) & embark on a new career as a full-time trader in 2007. As such, I do incorporate both FA & TA into my analysis, particularly when formulation my longer-term outlook for a stock, commodity or the financial markets.

As I’ve already exceed the length of my typical posts, I’m going to let the charts below do the rest of the talking but before that, I wanted to share the following link to this article from Reuters which opens with: “The Federal Reserve on Tuesday delivered its starkest warning yet under Chair Janet Yellen that by its assessment U.S. stocks are pricey.” (click this link to view full article: Fed Warns U.S. Equity Valuations “Well Above” Median. It would appear to me that is Yellen’s way of trying to ‘talk-down’ the market in order to prevent a catastrophic meltdown once the Fed is soon force to embark on a meaningful (not token, like the last hike) & lasting cycle of rate hikes in order to prevent minimize the damage of once again being caught behind the curve as inflation begins a steady climb, as we’ve already seen with commodity prices exploding after putting in what clearly appears to be an end of their multi-year bear market earlier this year.

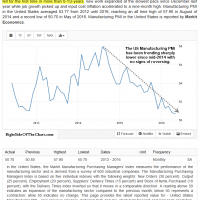

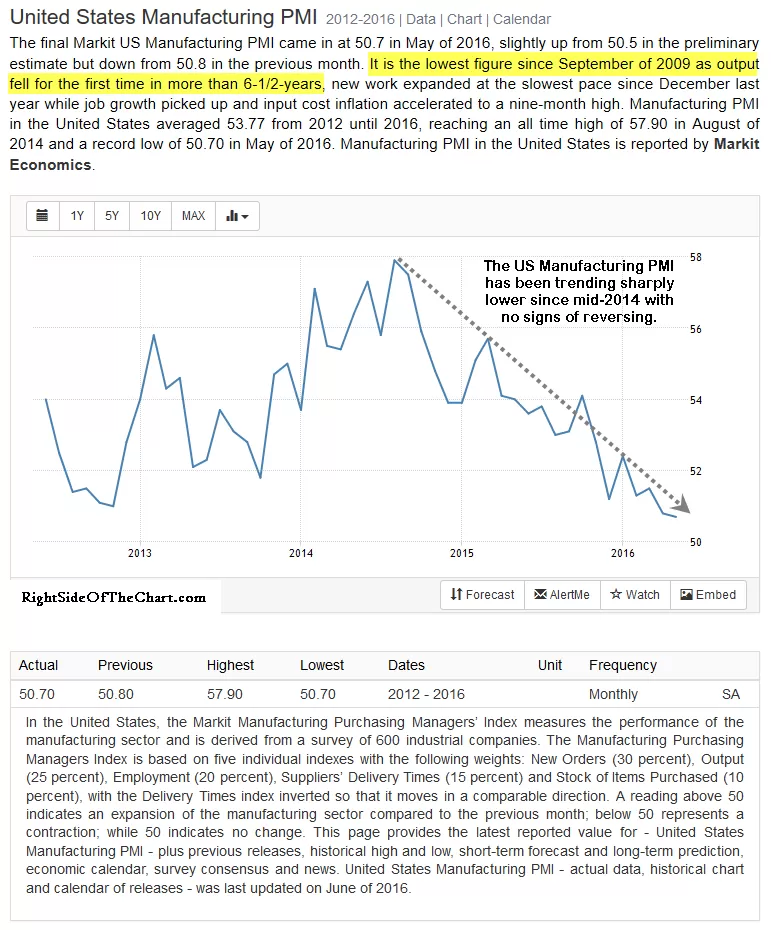

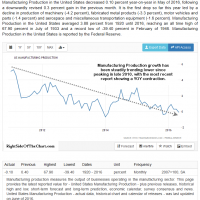

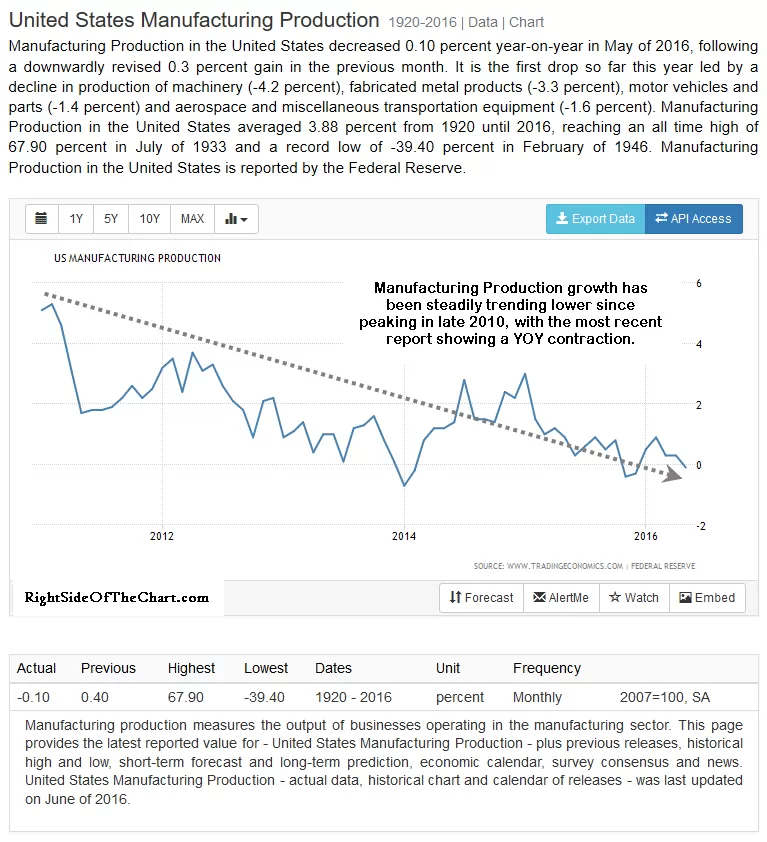

I’ve been making the case from a technical perspective for some time now that when the U.S. stock market peaked in early-to-mid 2015, that it was most likely the end of the bull market that kicked off with the March 2009 lows. The charts below, using fundamental analysis, help to corroborate the bearish technical case as many of these economic indicators also peaked around the same time, with most if not all showing continued deterioration since without any signs of reversing trend. Click on the first chart in a series to expand, then click the arrow to the right to advance to the next full-sized chart.

-

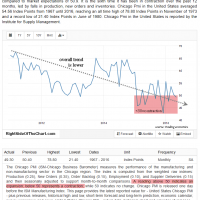

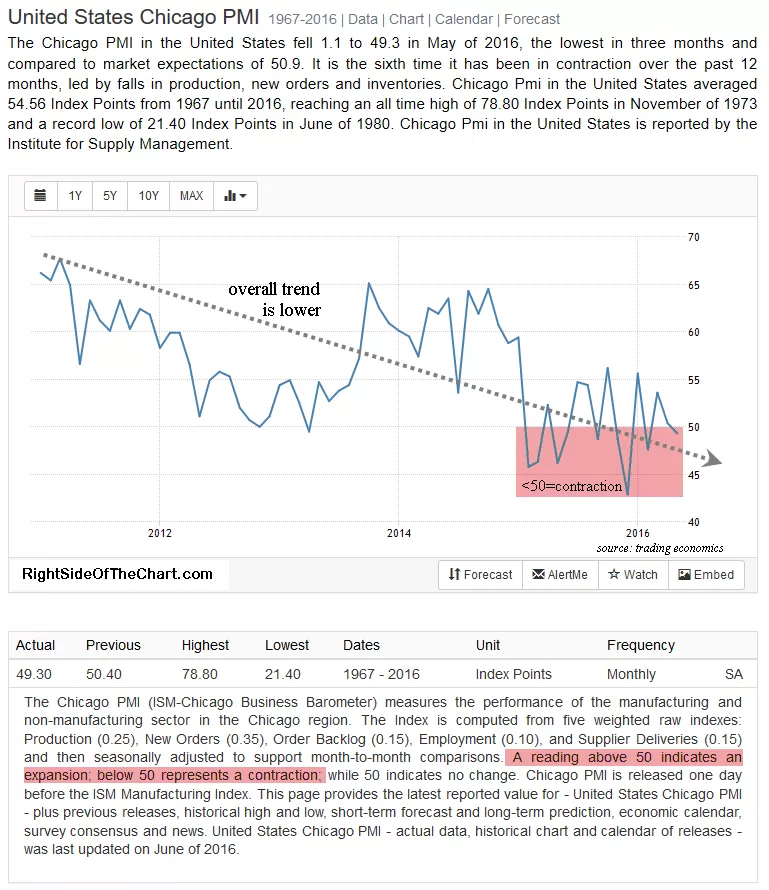

- Chicago PMI May 2016

-

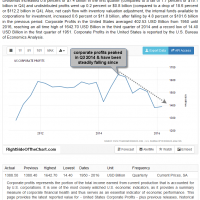

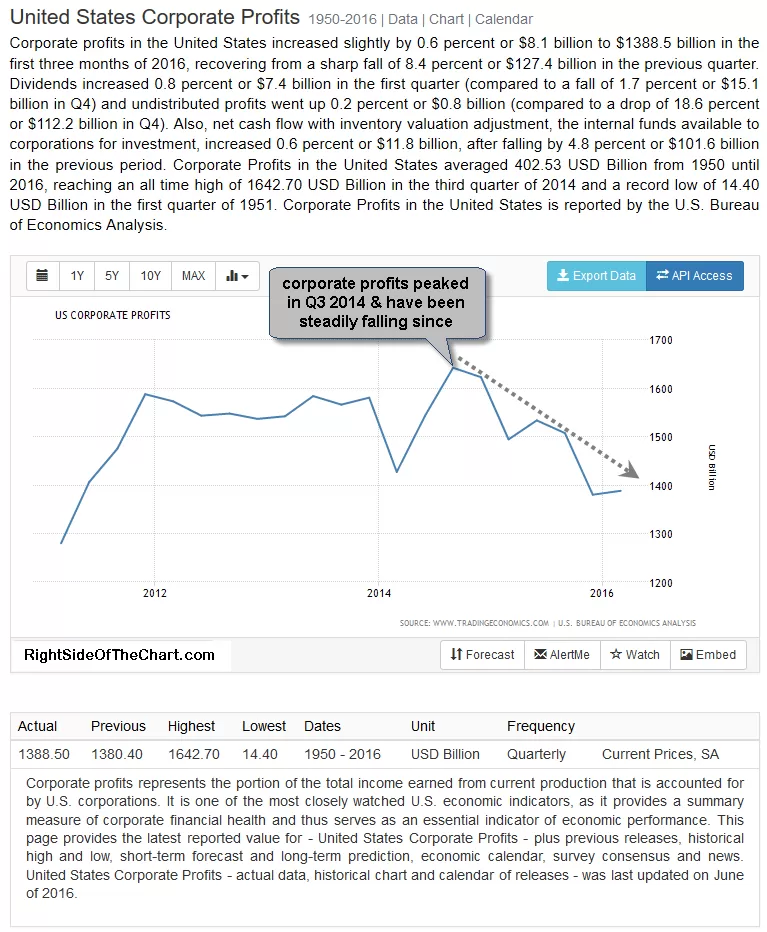

- Corporate Profits Q1 2016

-

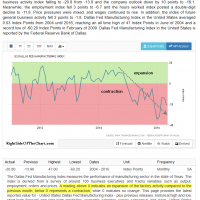

- Dallas Fed Manufacturing Index May ’16

-

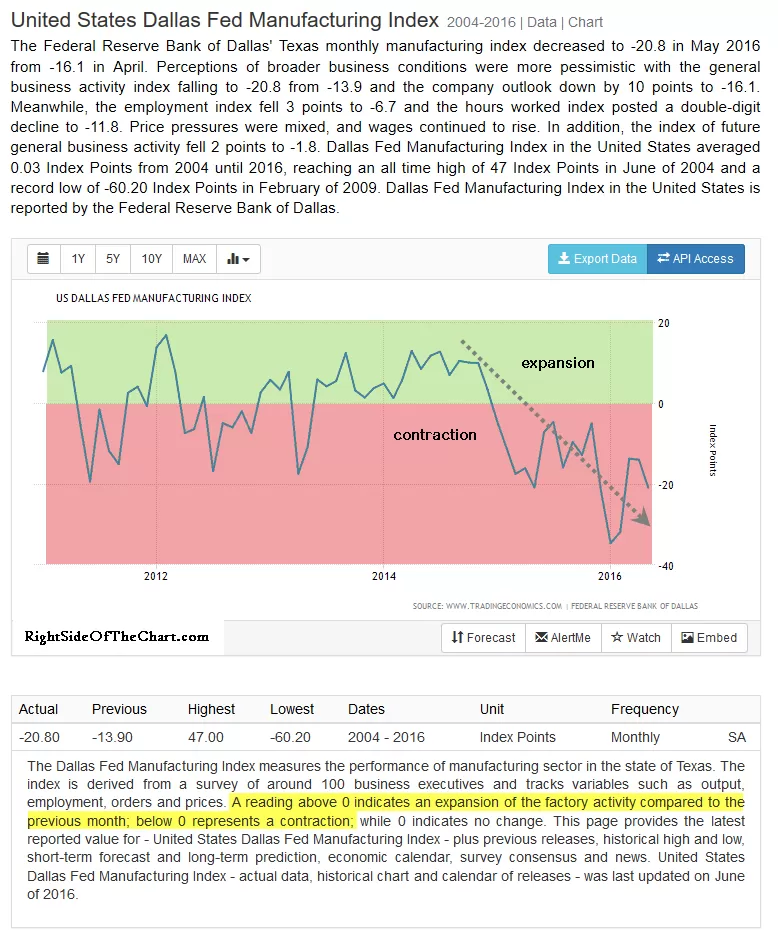

- Industrial Production May 2016

-

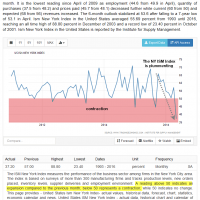

- ISM NY Index May 2016

-

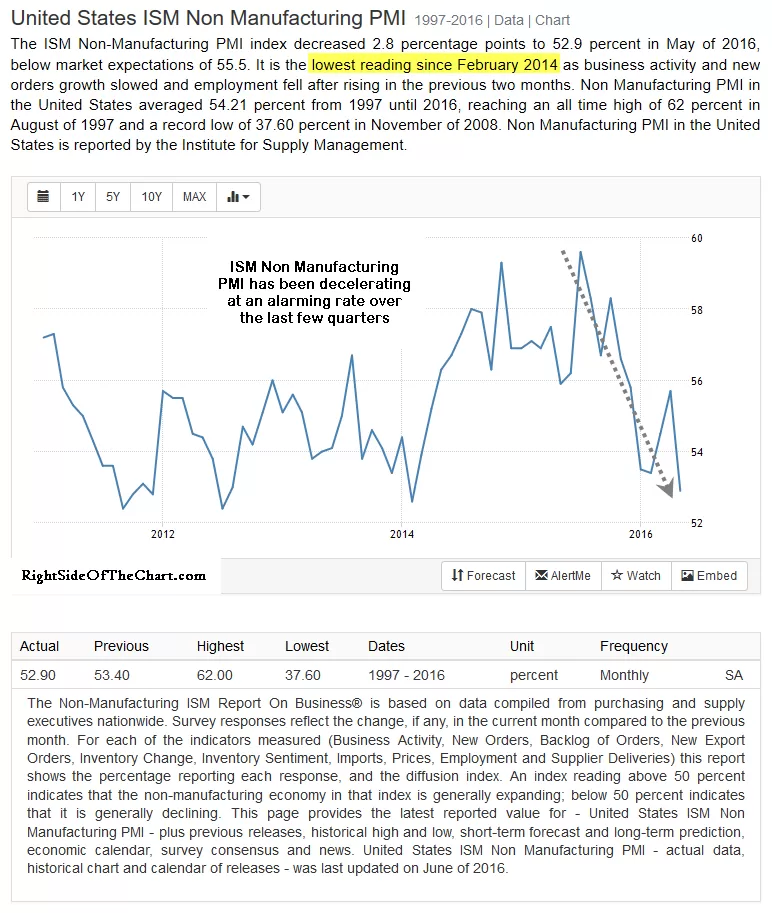

- ISM Non Manufacturing PMI May 2016

-

- Manufacturing PMI May 2016

-

- Manufacturing Production May 2016

-

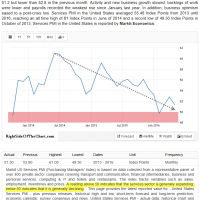

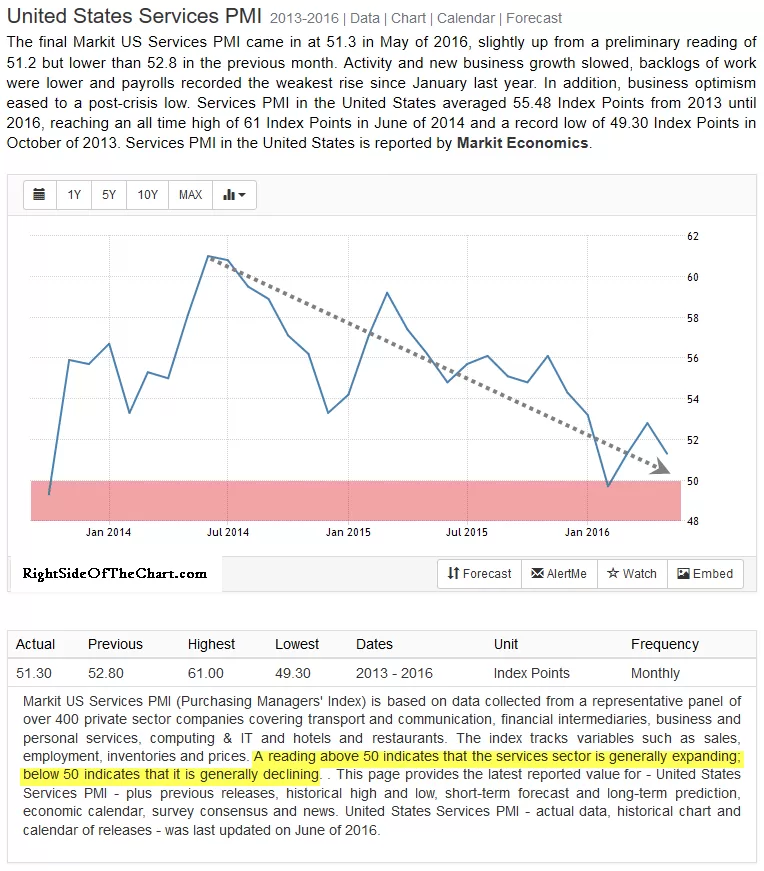

- Services PMI May 2016

-

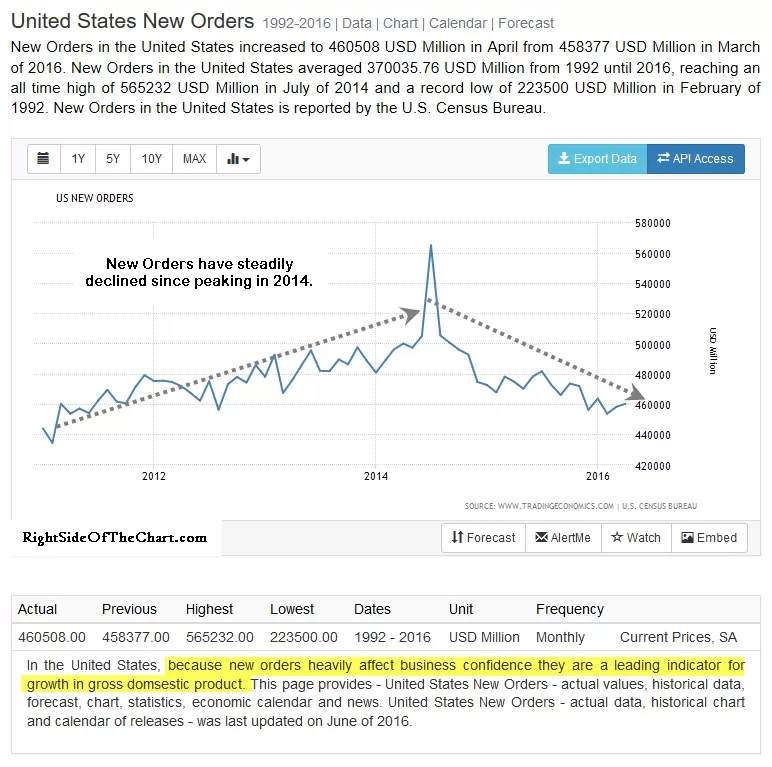

- New Orders April 2016

-

- S&P 500 Real Earning Growth

-

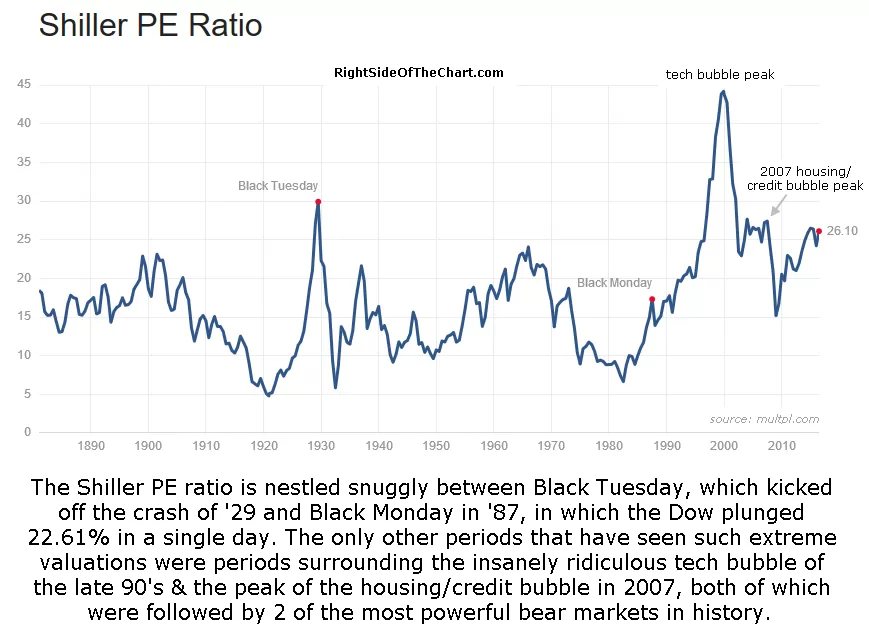

- Shiller PE Ratio June 22, 2016

-

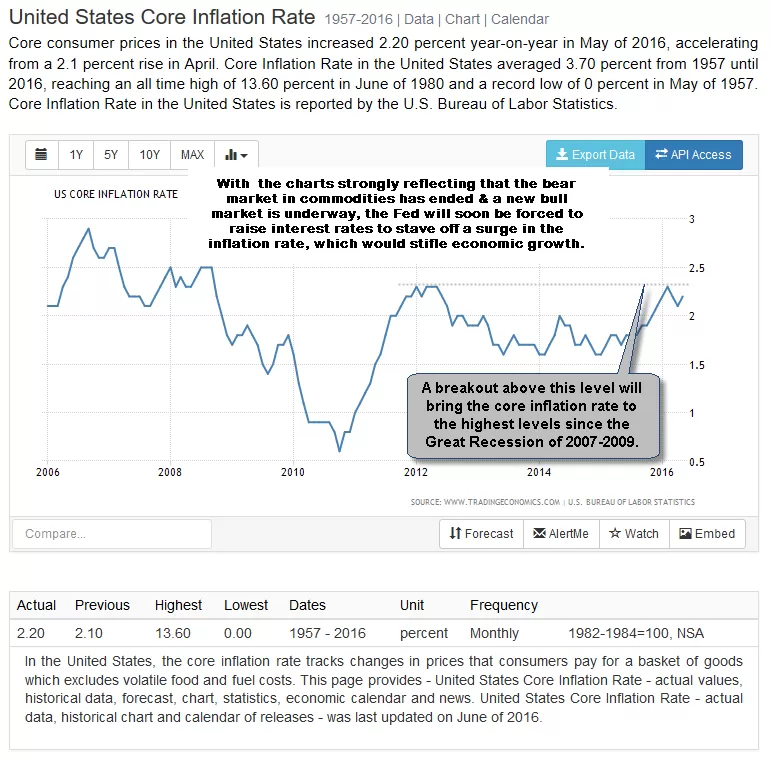

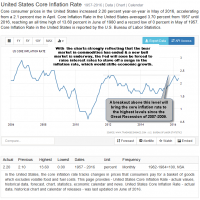

- Core Inflation Rate May 2016