My commentary on the broad market has been unusually light in recent weeks as I’ve had little interest or desire to trade typical equities, other than a couple of recent short trades, instead focusing on select commodities & precious metals. Although I haven’t posted many updated charts lately, I have kept the US broad market charts ($SPX, $COMP, $RUT, etc…) found on the Live Charts page updated. In doing so, I’ve been monitoring what appears to be a possible broadening top, aka- megaphone pattern in the S&P500 as well as some other large caps indices such as the DJ Composite and the Wilshire 5000 Composite Index.

-

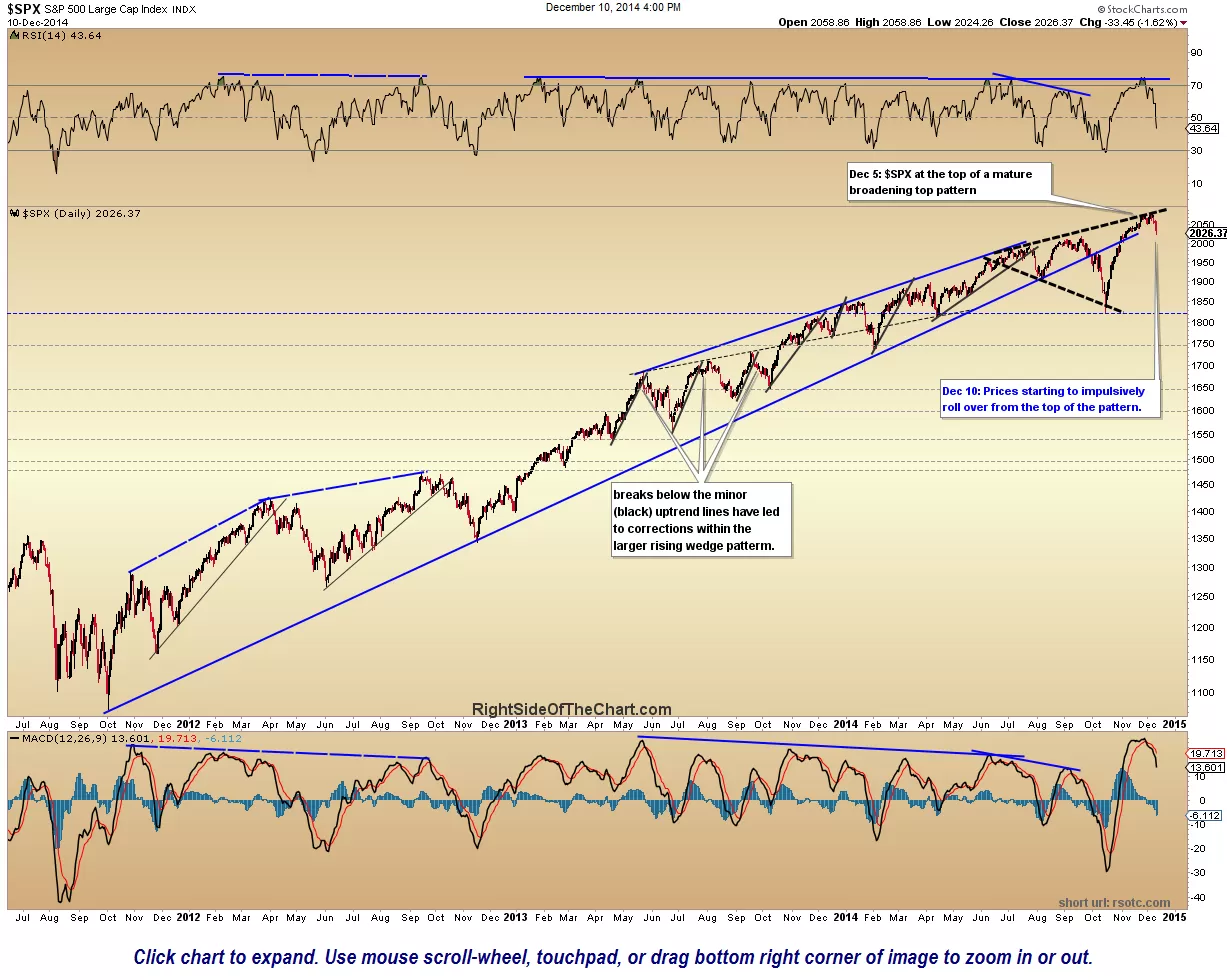

- $SPX daily Dec 10th

-

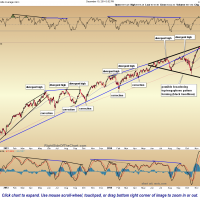

- $DJA daily Dec 10th

-

- $RUT daily Dec 10th

-

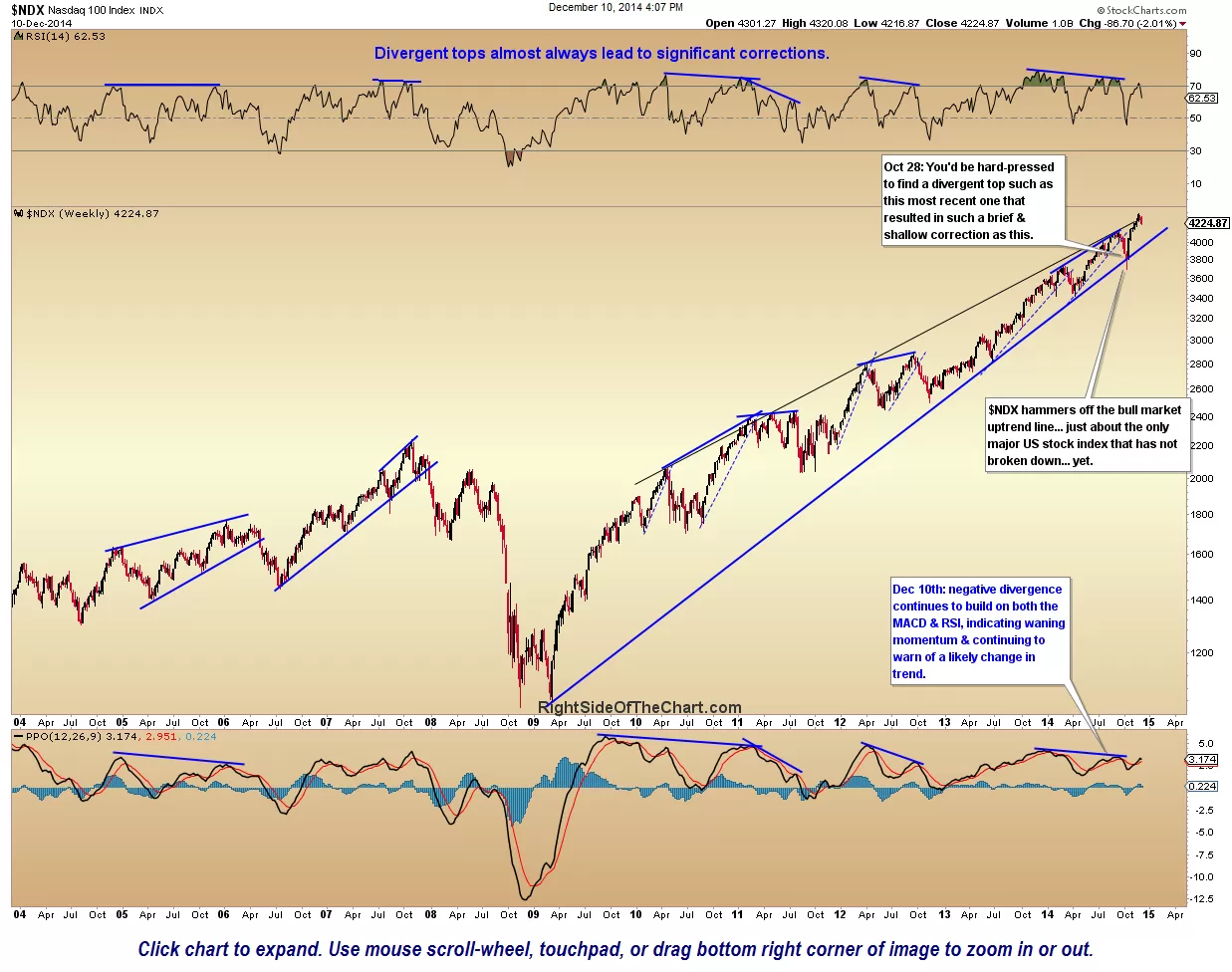

- $NDX weekly Dec 10th

The recent price action over the last couple of trading sessions has helped to validate those potential topping patterns as prices have begun to impulsively roll over after the third (which is often the final) tag of the top of the pattern. Given, there is still a lot of work to be done technically to make a case for a lasting trend reversal but despite the cheers from the mainstream media that cite cheap oil as the latest reason to extend this aging bull market, I’m still not buying it.

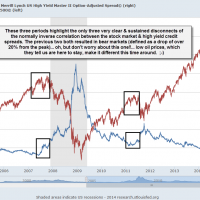

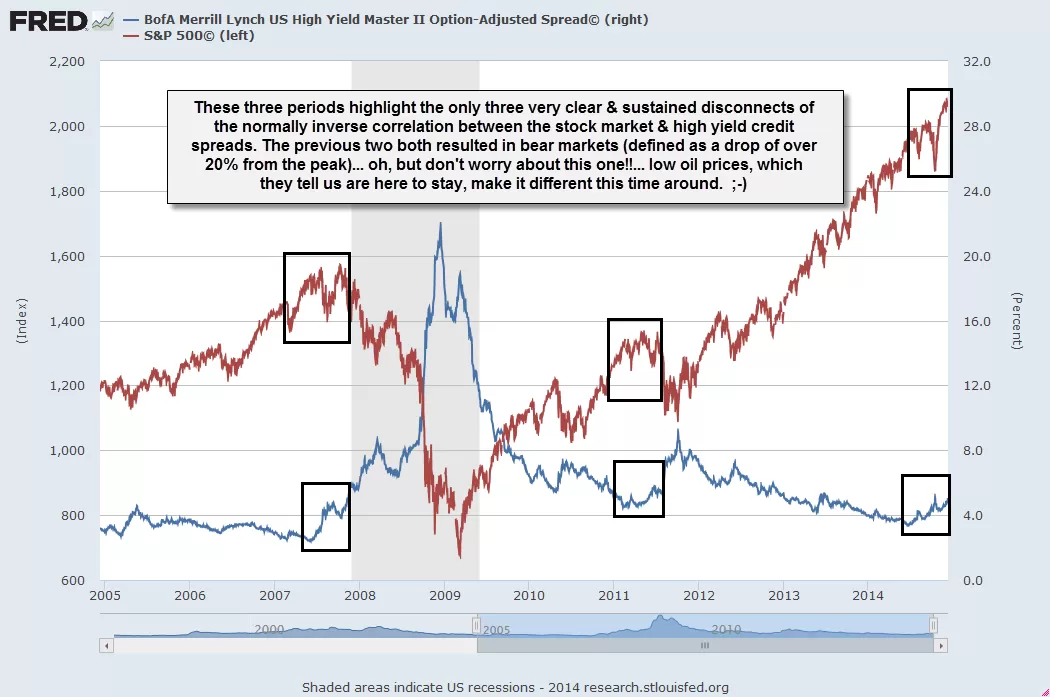

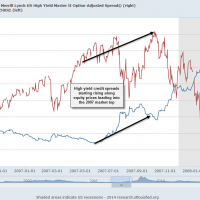

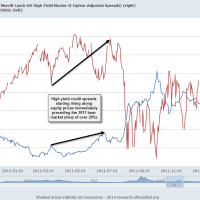

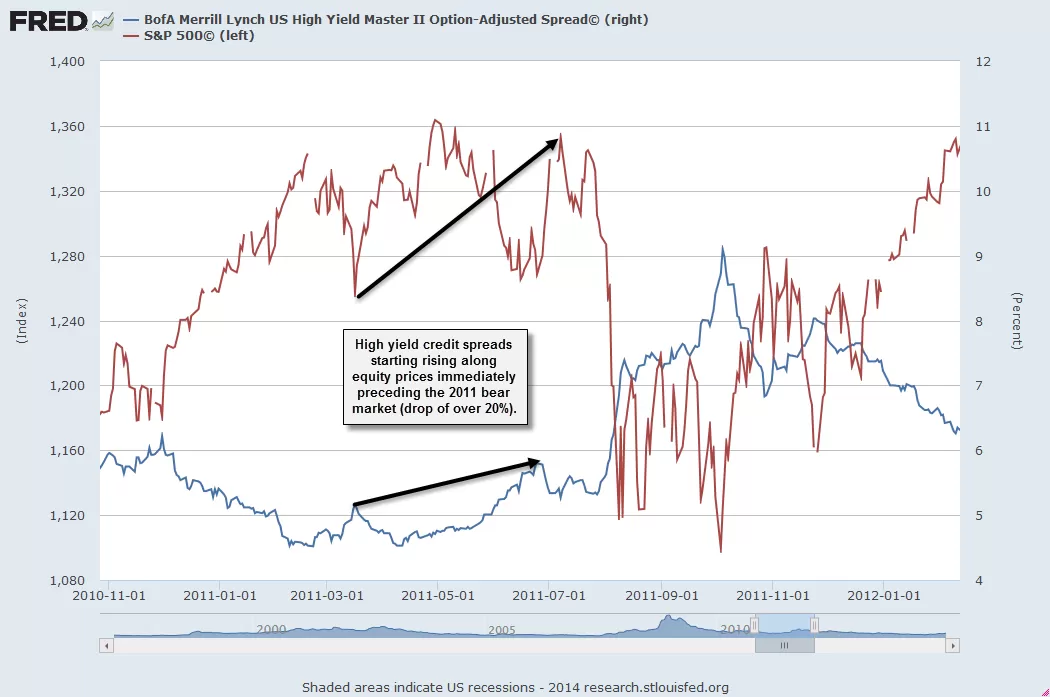

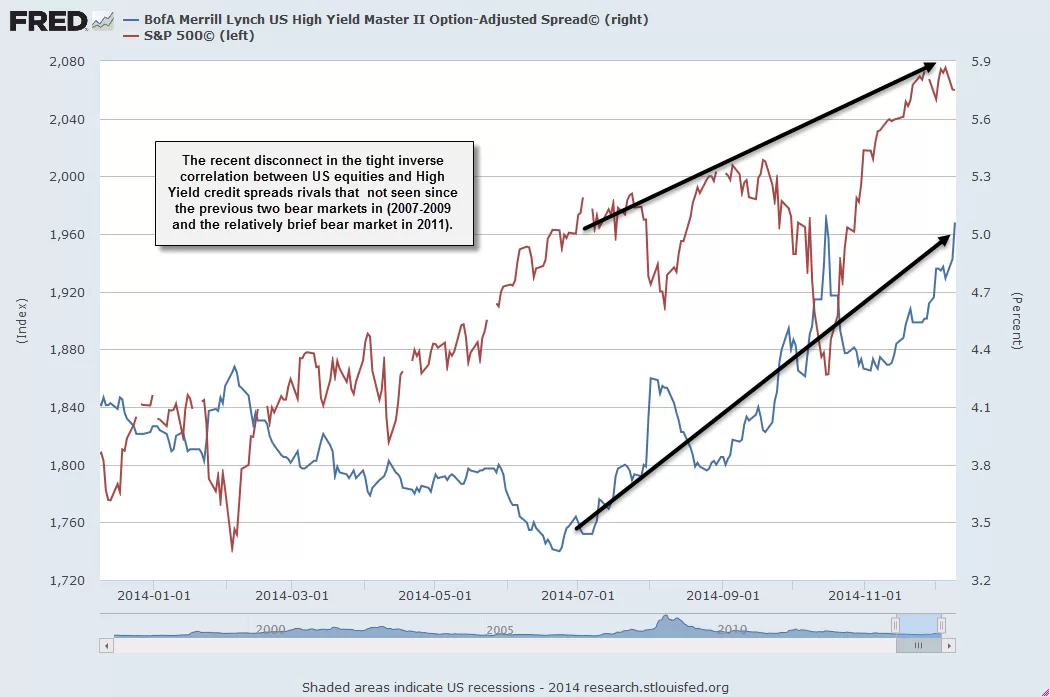

In addition to the recently discussed deterioration in the market internals from the Dec 2nd “Extreme Market Breadth Divergences Persist post, I also continue to monitor the building divergence… or more accurately, convergence or unusual correlation, between US Equities and High Yield Credit Spreads. This is another rare but fairly reliable indicator that although all seems rosy in the stock market & the economy, there may be substantial problems brewing under the hood. The chart of the $SPX vs. JNK shows the historically tight correlation between US stock prices and junk bond prices while highlighting the recent disconnect or divergence between the two. The JNK vs. TLT chart highlights the recent plunge in high yield bond prices, despite both a rising stock market AND falling interest rates (hence, TLT has risen in price).

Some of divergence between the two may also be attributed to a flight-to-safety but with the stock market printing new all-time highs, there is a major disconnect somewhere as normally, stocks are sold while treasuries when investors are concerned about risk. Are the credit markets over-reacting or is the stock market ignoring some deterioration in fundamentals or some other underlying risk that is getting buried under the “cheap oil!!” headlines? Maybe it’s neither and simply one more in a long line of central bank induced distortions in the financial markets that will ultimately dissipate or moderate through a reversion to the mean (e.g.- stock trade flat for a while while credit spreads moderate). Only time will tell but until these abnormal & potentially ominous developments in the credit markets disappear, the potential for a significant (10%+) drop in equities remains elevated at this time.

-

- 10 year Credit Spreads vs. SPX

-

- 2007 Credit Spreads vs. SPX

-

- 2011 Credit Spread vs. SPX

-

- 2014 Credit Spreads vs. SPX

-

- $SPX vs. JNK Dec 10th

-

- JNK vs. TLT