On the chart below, I plotted the month-end values of the S&P 500 against the Domestic (U.S.) Long-term Equity-Only Mutual Fund Flows. Although we don’t have the data for the October month end yet, the first two weekly reporting periods (Oct 7th & Oct 14th) for Domestic Equity Funds have seen net outflows of -$1.31 & -$1.44 billion, respectively, for a total of roughly $2.8 billion in net outflows MTD (data for the week ending Oct 21st should be released in the next day or two).

Note how investors “bought the dip” in previous corrections, providing institutions with the capital to buy more stocks which fueled the next leg higher in U.S. equities whereas this most recent correction has been followed by persistent, massive withdrawals from US equity funds.

$SPX vs Fund Flows Oct 27th

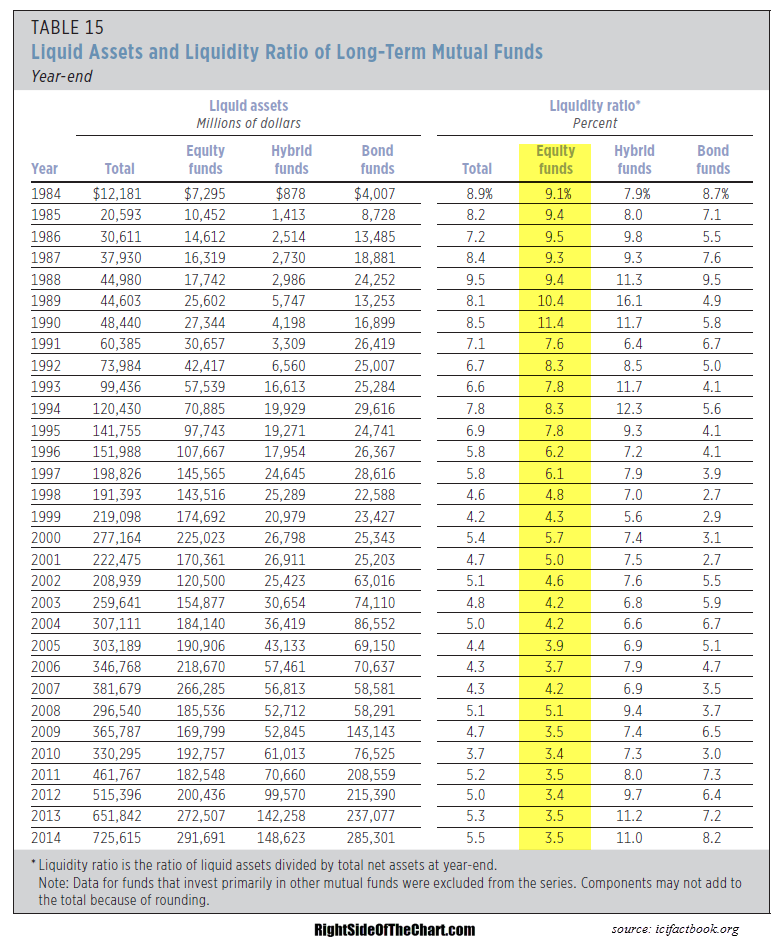

Should this trend of outflows, which is by far, the largest amount of net outflows from US stock funds in years, continue or more accurately, not reverse soon, with new money coming back to those institutions, many mutual funds will be forced to liquidate holdings in order to meet redemptions. With the equity funds recently running at historically low liquidity ratios (3.4% at the end of August, the most recent data that I was able to find & looking at those withdrawals since, I really doubt that figure has increased), coupled with the fact that despite the recent selloff, margin debt remains near historical highs, the risk of a waterfall type selloff remains quite elevated at this time.

Historical Liquidity Ratios