A few months ago I made a case that a correction in the US was likely. That prediction couldn’t have proved to be more wrong as the dollar just sliced through a key resistance level and burned through divergences & overbought levels as if they weren’t even there…. an extremely rare occurrence. My only saving grace on getting that call so wrong heading into the end of last year was the fact that I rarely ever trade currencies and the extensive analysis that was posted around that time was to support the bullish outlook for gold & precious metal stocks at the time. As I like to say; better to be right for the wrong reasons than wrong for the right reasons as gold & the mining sector had an extremely lucrative run leading into the last few months of the year and well into January.

As the post-financial meltdown, QE driven market over the last few years is one marked by extremes and unusual disconnects, that rally in precious metals was one of those rare disconnects between gold prices and the US Dollar ($USD), which typically have a relatively tight inverse correlation (i.e.- dollar up = gold down). Of course the rally in gold & precious metal stocks, despite the unstoppable run in the dollar, wasn’t dumb luck either, as a very solid bullish technical case was made for gold & the mining sector at the time.

With that being said, disconnects from historical price relationships don’t last forever and at some point, such as we’ve seen over the last couple of months, the rising dollar will (and just recently has) taken its toll on gold prices. Of course, that relationship cuts both ways as when that long overdue correction in the $USD finally does begin to take hold, there is a very good chance, IMO, that gold prices will rally as the dollar falls. It might be easy to say that if I were a perma-gold bug (which I am not, just as comfortable shorting gold & gold stocks as I am going long), but the primary reasoning behind my belief that gold will rally during the next correction in the dollar is exactly for the same reason that gold has held up so well despite a near-parabolic rise in the dollar over the last 8+ months. That tells me that in spite of the usually inverse correlation between gold price & the US dollar, there as been a resilient bid beneath gold prices as, since June 4, 2014, the dollar has soared an impressive 21% yet gold prices have only fallen about 6 1/2% over the same time period.

For example, from the week of March 7, 2008 thru Oct 31, 2008, the $USD made an nearly identical vertical rise compared to the most recent rally, climbing 24% in about 8 months. Since June 3rd, 9 months ago, the $USD has climbed about 21% while gold has only fallen a relatively minor 6 1/2% (and only 4% before the big gap down on Friday). Such resiliency for gold prices in spite of a parabolic, nearly unprecedented rise in the dollar speaks volumes to the supply/demand dynamics IMO and when factoring in the longer-term bullish technical case that I’ve been making for months now, PLUS the fact that gold prices are fresh off a 40%, multi-year bear market, that bodes well for the intermediate & longer-term outlook for gold, especially if/when the $USD reverses trend.

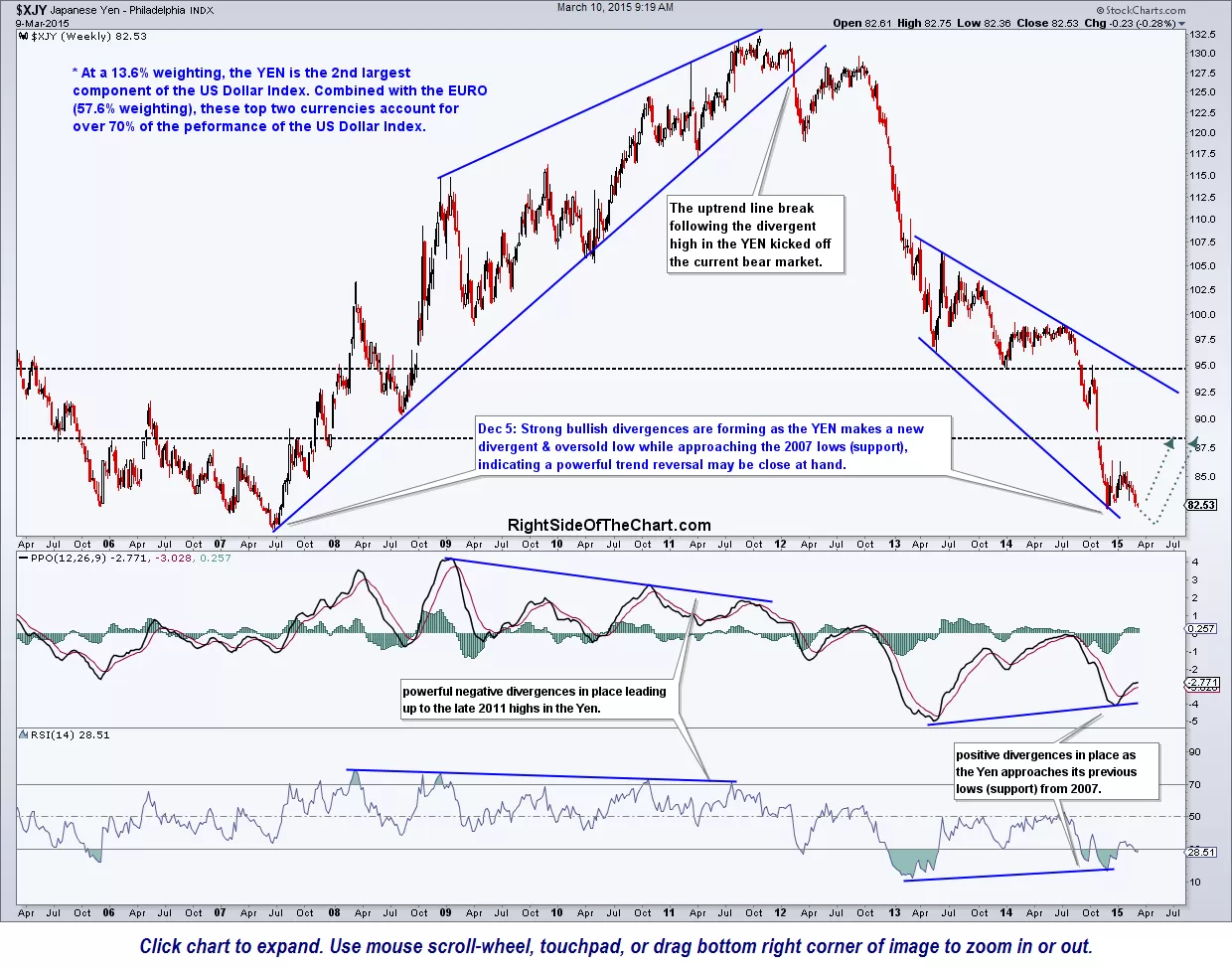

On a final note, I would be remiss not to point out the correlation with US stock prices and the $USD. I don’t believe it is a coincidence that the first short on the US stock indices that I’ve made this year coincides with a pullback that I am expecting in the US Dollar. With that being said, here are some daily & weekly charts on the $USD as well as the two currencies, the Euro & Yen, that comprise the bulk of the US Dollar Index. In other words, where they go, the dollar goes (the other way) and vice versa.

-

- $USD 20 yr weekly March 10th

-

- $USD daily March 10th

-

- $XEU 20 year weekly March

-

- $XJY weekly March 10th